Most FIRE plans are a fantasy. Here’s one that’s actually realistic.

Tired of FIRE advice that only works on paper? Here’s a more realistic view for financial independence that actually works, especially if you’re starting from zero.

Most FIRE plans sound amazing, until you try to follow one in real life.

They assume you’re single, childless, living in a low-cost area, with zero financial emergencies and a perfect 10% return forever.

Oh, and let’s not forget the infamous 4% rule... because markets never crash and life is always stable, right?

If you’ve ever read a FIRE blog and thought, “Cool story, but this has nothing to do with my life, you’re not alone.

Let me show you what a realistic FIRE path actually looks like. One that works when life hits hard, markets wobble, and you don’t have $100k sitting around.

Before I break it down, I want to hear from you.

I know everyone’s on a different path, and I’m curious—what’s actually making this hard for you right now?

Quick poll

What’s wrong with most FIRE plans?

They rely on ideal conditions.

They assume you’ll never lose your job, get sick, have kids, or make mistakes.

They downplay taxes, inflation, and sequence risk.

They pretend you can coast to freedom with $200/month into an ETF.

Reality check: Most people don’t have 30 years of perfect investing behavior in them. Life will punch you in the face.

A Realistic FIRE approach (especially if you’re starting from scratch)

This is what I’ve done, and what actually works:

1. Increase income first

FIRE is 90% offense. You can’t save your way to freedom with low income.

Build something of your own. Start small. A side hustle. A freelance gig. Learn how to make your money work for you instead of the other way around. Because when your job is your only source of income, you’re not “secure.” You’re just exposed.

Right now, I have 3 income streams that I use to fuel my dream of buying back my freedom.

The first is my full-time job.

Then there’s my swing trading system, which gives me weekly opportunities, and you can take advantage of them too if you join the community.

The third is the two websites I own, which bring in ad revenue.

None of these take up a ton of my weekly time, that’s how I’m able to do it while still working full-time. But it didn’t happen overnight.

It took me years to build this.

It might not take you years like it did for me, but be ready to put in the time.

If it were easy, everyone would be doing it.

Just remember this: focus on increasing your income, not lowering your quality of life just to save an extra fifty bucks.

2. Keep expenses simple, not extreme

After I lost everything in 2021 when COVID hit, it took me 6 months to get back up.

Not financially, but mentally.

Since I turned 26, every single dollar I’ve made has gone into the capital markets, into investing, and into trading.

The only thing I want to buy is freedom.

I don’t care about anything else.

I’m not interested in impressing your friends with the latest car.

When I was a kid, I used to say I’d buy an Audi R8. Guess what? I can afford that R8 now.

But if I have to trade my freedom for it, if it pulls me further from my dream—then it’s not worth it.

For what?

To impress a friend who probably doesn’t care? To spark envy that adds zero value to my life?

I’m still using an iPhone 11. The latest one is iPhone 16.

Does it still work? Yeah. You get the point.

Cut your costs, sure, but don’t sacrifice your well-being or your health.

You don’t need to live like a monk. Just avoid lifestyle creep. Be intentional, not miserable.

3. Invest aggressively while you’re young

Forget the 60/40 portfolio in your 20s. You need asymmetric bets when your downside is low. Growth stocks, momentum trading, crypto (with risk management).

They teach you to just invest in a single ETF until you’re 65 and maybe hit FIRE.

Yeah, that might work for 90% of people. But not for you.

If you’re the kind of person who reads about investing, who studies swing trading, you’re built different. You have to approach this differently.

You’re here to trade discomfort for freedom.

That means doing what the crowd isn’t.

That means showing up when no one’s watching.

4. Build flexibility, not just a number

Don’t chase “$1M and done.” Chase the ability to say no, to pivot, to take sabbaticals, to work on your terms.

FIRE isn’t about hitting a magic number and doing nothing ever again.

No. You’ll be bored out of your mind within a month if you don’t have a purpose.

And guess what you’ll do?

You’ll spend. You’ll drown in distractions and pleasures.

Prepare for that..mentally.

Build your own routine, your own mission, before the freedom comes.

And that starts with you, who you are, not just what you earn.

5. Reinvest wins.

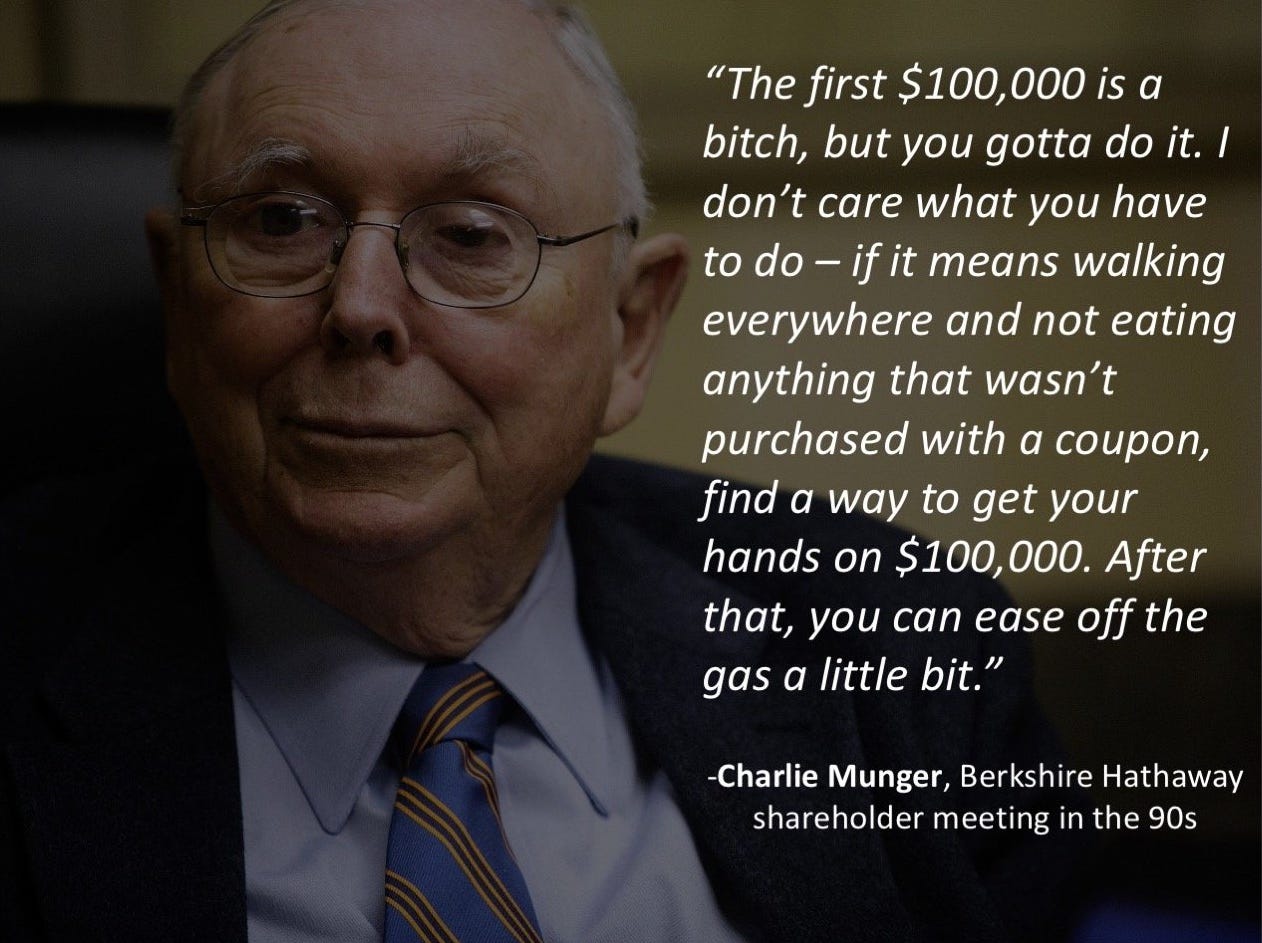

Charlie Munger said:

“The first $100,000 is a b*tch, but you gotta do it.”

And he was right.

After that, money starts working for you.

Until then, you work for every single dollar.

In the beginning, if you manage to hit an asymmetric play, turn $1,000 into $10,000 on some biotech stock or crypto move, lock in that trade. (I do not recommend this type of gambling)

Don’t fall into the trap of thinking “this is going to a million.”

That’s how profits vanish :greed.

At this stage, every dollar counts. You need to start compounding something, not dreaming about 100x gains.

So if you’re lucky enough to land a 10x early on, take it and run.

Early gains are rocket fuel. Compound them. Don’t sabotage your own runway.

It’s not about retiring at 35 with a hammock and a coconut. It’s about building optionality, as fast and as realistically as possible.

The Mindset shift most people miss

FIRE isn’t a number.

It’s not even really about money.

It’s about freedom and control.

The faster you earn back control of your time, energy, and decisions, the closer you are to financial independence. And that might happen way before your net worth hits seven figures.

In this community, before we talk about making money, we will define your plan, clearly.

We’ll start by answering some fundamental questions:

Why do you want to make this money?

The answer has to mean something to you. It has to be written in bold, with commas and periods.

If it’s not strong enough, it won’t carry you through the hard times.

Then we’ll start building a personal plan, based on your income, your expenses, your age, and your end goal.

I want to help as many people as possible figure this out, or at the very least, gain clarity and structure around their path.

So if that sounds like something you need, hit subscribe and I’ll see you inside the community.

And feel free to reach out.

Drop a comment and tell me what your version of financial freedom looks like.

Let’s kill the fantasy and build something real.